While most of America, by now, may know about the existence of shale gas and Fracking, most do not know that the de facto energy plan of the US is an increased reliance on LNG (liquified natural gas) and that most of this LNG will have to be imported.

In terms of needed infrastructure, this means that the US needs

to develop significantly more LNG importation and processing facilities to meet this goal. The goal is mostly idiotic in that

a) it continues our use of fossil fuels and b) it provides us some time relief so that we can further delay the needed investments in alternative and renewable sources of energy and electricity generation.

This coming LNG economy is perhaps the most under reported big story in America although there are a few informative reports

now on this issue:

The LNG Energy Economy.

The most up to data analysis of this situation can be found

here

But don't worry, everything will be alright

Most importation facilities, like the proposed one at Coos Bay, would be located on the coastline at places where there is fairly

ready access to the existing pipe line network in the US (which is quite extensive).

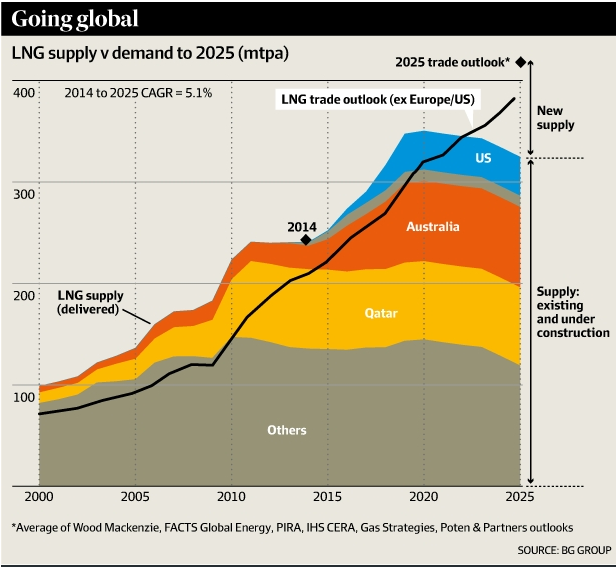

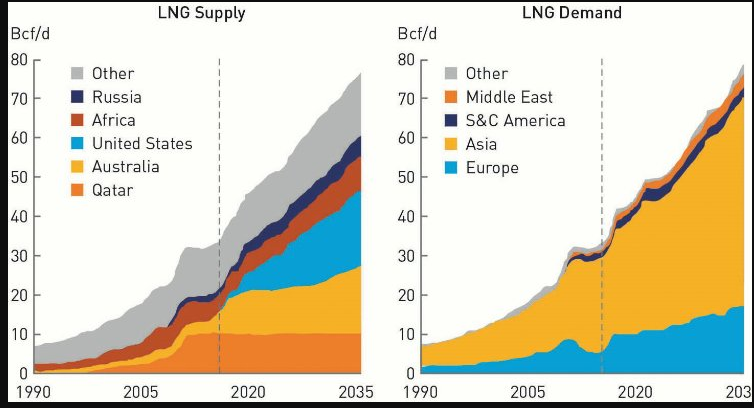

There are many available projections about the near term future growth but, at the moment, the use of LNG is the fastest growing energy technology in the world. This is NOT Green:

The doubling time is about 10-15 years at the moment:

Canada regular NG Imports are in decline: The implicit plan is that LNG imports will magically appear

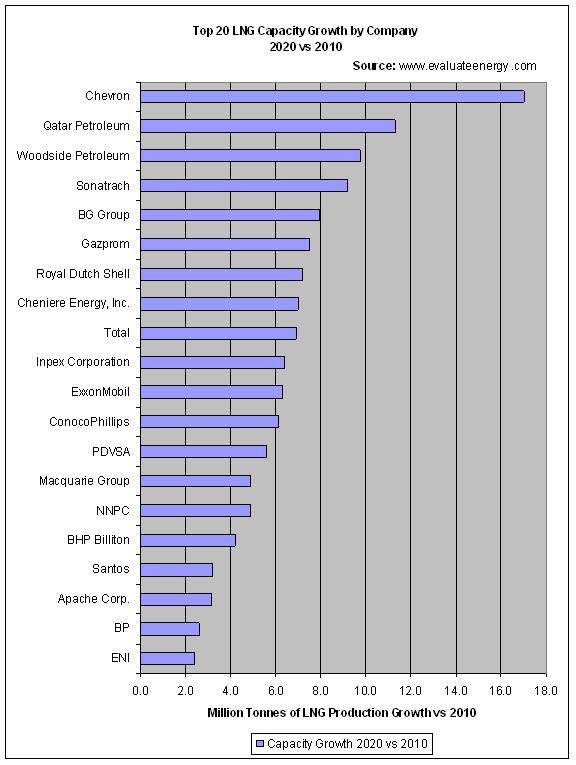

And Chevron has the boldest plans:

There are a lot of world politics potentially involved with who

gets the gas and who gets the gas from whom. The situation is quite volatile and can change dramatically in just a few months (e.g. currently the US gets no gas from Qatar).

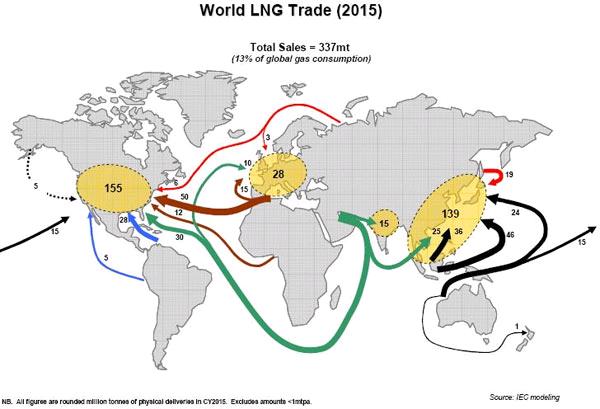

The latest world summary is here

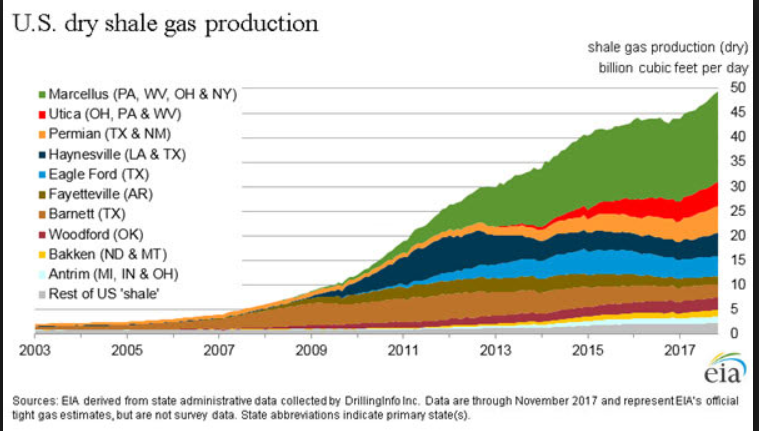

Currently increasing domestic production is reducing needs for imports although that production may be levelling off some.

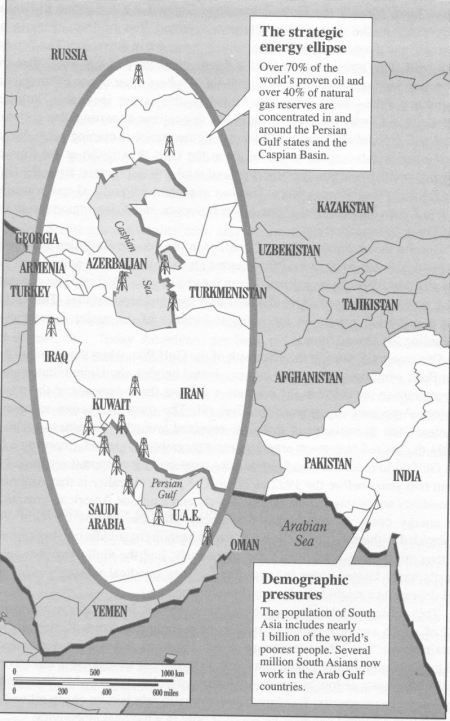

The Strategic Ellipse

The overall delivery chain of LNG consists of a small number

of steps which lends itself to subsequent distribution via pipeline infrastructure, once step 3 is accomplished.

The overall delivery chain of LNG consists of a small number

of steps which lends itself to subsequent distribution via pipeline infrastructure, once step 3 is accomplished.

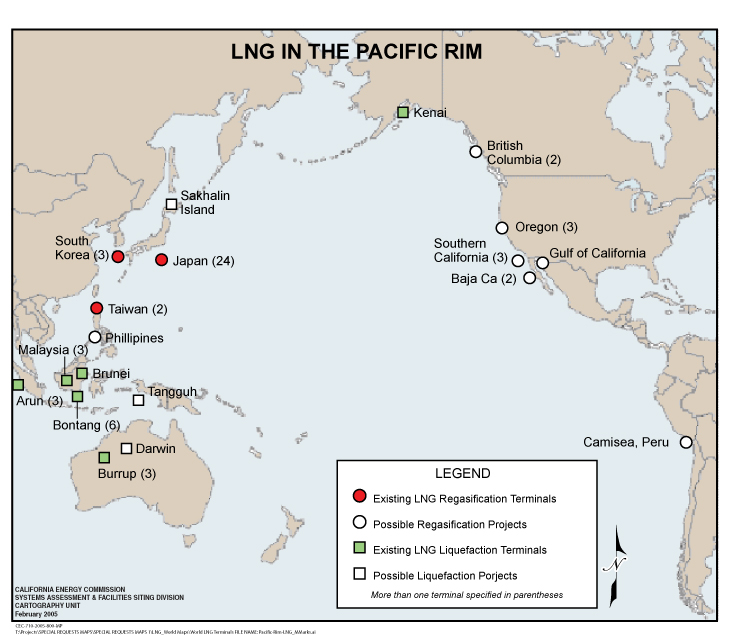

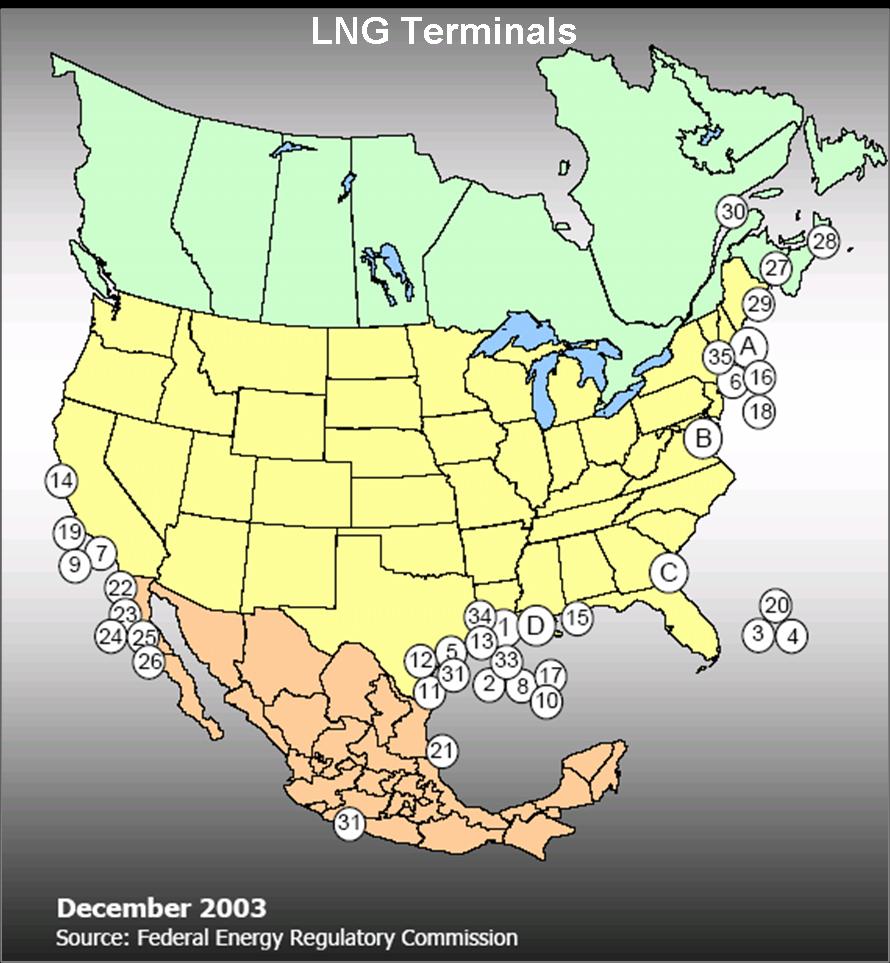

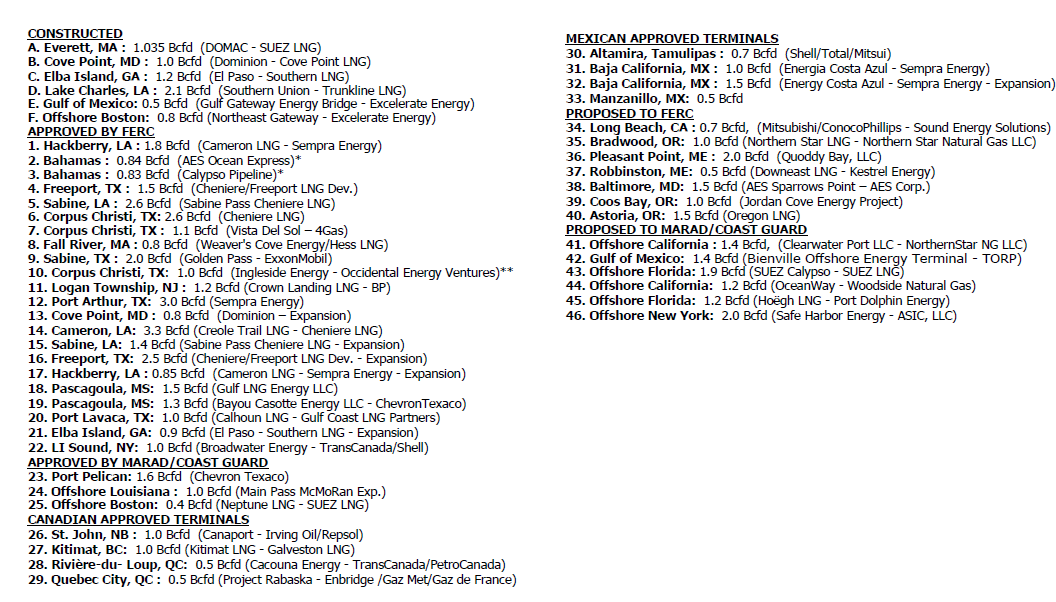

The sequence of images below show a) our current LNG import structure in the US, b) the situation on the pacific rim which is completely dominated by Japan (24 facilities) who has bet their future on the

availability of ready availability of LNG c) the planned situation in the US, which

will dwarf Japan, making the US the largest consumer of LNG. This is completely at odds with one of our stated goals which is "energy independence" - but this is what is happening in the real world!

|